Last May, Title III of the JOBs Act was passed, too much fanfare from the public. Known as the CROWDFUND Act the latest addition to the Jumpstart Our Business Startups Act, Title III, grants unaccredited investors (net worth < $1 million or annual income < $200,000) the ability to invest and purchase equity or debt in private companies, explicitly start-ups. With the passage of Title III and Regulation CF, Crowdfund, investing has truly become democratized, into people-powered finance.

How Crowdfunding Has Changed Investment

The concept of crowdfunding has revolutionized the start-up industry. In the past access to capital was sorted into two blocks. ”Friends and Family” in one end of the investor sophistication spectrum with “professional” Angel Investors (accredited investors looking to support a project) and Venture Capital firms on the other.

Until crowdfunding, a significant gap existed between the two levels of funding that many companies couldn't cross without preparation or money to advance through the pitching process. Thus, the prominence of sites including Indiegogo, Gofundme, and SeedInvest has created unprecedented opportunities for the entrepreneur through two main benefits:

- Solicit financing or investment by simply posting appealing concepts to develop: a simple platform where it's easy to submit ideas without the barrier of prototyping.

- Access to an ever-growing base of investors or supporters actively seeking new projects.

Crowdfunding has lowered the barrier and enabled the “crowd” to financially support directly with the company.

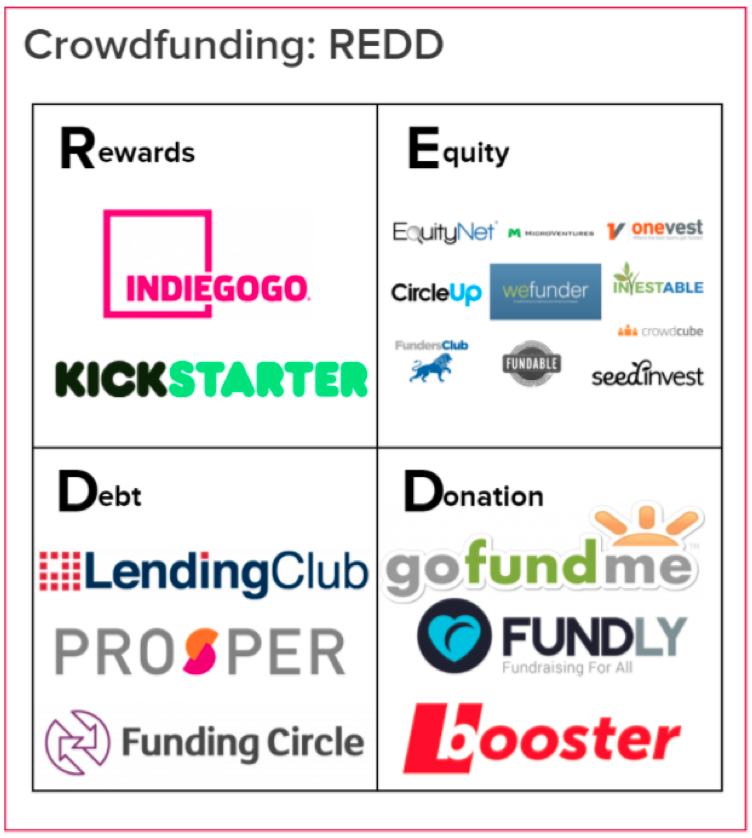

REDD - Breaking Down Crowdfunding

Crowdfunding in its most basic sense can be split into four categories: Rewards, Equity, Debt, Donation (REDD).

R - Rewards: "You give me money, and in exchange, I will give you a special reward for your financial support (ie: special price, early access"

E - Equity: “You give me money, I will give you a % of ownership in the company.”

D - Debt: You lend me money, I’ll pay you back with interest.

D - Donation: Give me money, no strings attached, and support a cause.

Reward-based crowdfunding was the first type of crowdfunding to emerge. Starting in 2008, platforms such as Indiegogo and Kickstarter have allowed companies to directly raise capital from the consumer with little expected return except for “rewards” and the promise of product that will hopefully be produced. Of course, campaigns offer a pre-order discount and other smaller incentives including other products or accessories for various tiers of support. However, at the most general level until there's a product there's little else to back the campaign, many of which take months to years to complete production. Nevertheless, the success of rewards-based crowdfunding has demonstrated both accredited and non-accredited investors have the interest in supporting a company achieves its goals with little benefit to themselves. Since 2008, Indiegogo and Kickstarter have raised over $4 billion in capital and have been host to over 500,000 projects.

Donation based crowdfunding came out of the incredible successes of the first crowdfunding platforms. GoFundMe, the pioneer of this category, has allowed thousands of campaigns to succeed that may not have otherwise. There is essentially no return for the donor except faith in the campaign's use of their money. But GoFundMe and similar platforms have shown the power of the internet to attract attention, disseminate information, and connect people. As of June 2017, Gofundme has raised over $3 billion and successfully changed the lives of millions

Logically taking rewards-based crowdfunding to the next step was Debt crowdfunding. Coming from the aftermath of the 2008 crash, Debt crowdfunding, commonly known as peer-to-peer (P2P) lending, was a way for companies to apply for loans. If accepted by the platform (most prominently Lending Club), they can borrow money from the crowd and in return pay interest back. P2P was simpler, quicker, and cheaper than from a bank due to lower overhead costs, interest rates, and wider audience. Debt crowdfunding has grown at a rapid rate, and now institutional investors like insurance companies and hedge funds play a major role, such that P2P is now referred to as “marketplace lending”. Debt crowdfunding has democratized the loan process for many, lowering the price barrier and entry point for funding. As of March 2017, Lending Club has issued over 2 million loans worth over $26 billion.

Finally, this leadup culminated in Equity crowdfunding. On such platforms, investors can purchase equity, debt, or other forms of securitized products (such as SAFE, or “simple agreement for future equity”, a type of convertible note) in private companies to support their growth. From rewards based crowdfunding, we see that people are willing to provide a project with capital, and as such should be enthusiastic in having an official stake in the success of a company through buying equity.

Because the nature of equity is much more complex, there are multiple regulations that govern equity crowdfunding to mitigate the risk for both parties (Founder of a venture and Investor of a venture). This takes us back to the JOBs Act and the passing of Regulation III, CF (Crowdfunding) last May.

Equity Crowdfunding: Regulations to Fit All

The JOBs Act (Jumpstart Our Business Startups Act) eases the regulations of securities (such as equity or debt) to allow equity crowdfunding by the SEC (Securities and Exchange Commission) through select exemptions. As of last May, there are three main Acts. It is important to note, however, that most equity crowdfunding platforms only offer their services in the allowance of one or two of these regulations.

Reg D or Title II, creates an exemption of Rule 506 and is split into Rule 506(b) and 506(c). As a whole, under Regulation D equity crowdfunding platforms can issue an unlimited amount of capital each offering but can only sell to accredited investors (which is not exactly the “crowd”.) Regulation D platforms are classified as crowdfunding mainly due to the access accredited investors and businesses have through online platforms.

Rule 506(b) allows up to 35 non-accredited investors but the offerings of securities are not allowed to be advertised. Investors can self certify that they are accredited.

Rule 506(c) allows only accredited investors and advertising is allowed. However, accredited status of investors must be verified (ex. A confirmation letter from a lawyer).

Reg A(+), or Title IV has two tiers. In both tiers non accredited and accredited investors to partake as well as the ability for advertisement. Tier I has a limit of $20 million per 12 month period and Tier II has a $50 million limit. However, if a company decides to go through with Reg A+ they must submit certain financial documents for review by the SEC for approval before the offering. Reg A (+) offerings are usually called mini IPO

Reg CF, the recently passed Title III is true equity crowdfunding. It allows any investor, regardless of status to participate with a minimum of $100 up to a $1 million limit depending on their net worth. The passage of Reg CF allows companies to avoid the scrutinization and reliance on the SEC and directly begin funding through a supported portal. With Reg CF, millions of potential investors now have the ability to participate.

As we can see, the JOBS act opened a new fundraising landscape with options for companies in different stages of development and investor relationsand startup strategy. It is complicated to understand the details of the regulations, so a good method is by looking at three examples of successful equity crowdfunding projects. A commonality between the three is that they all leveraged the success of a reward-based crowdfunding to help supplant equity-based crowdfunding.

At BEAST. We navigate the startup funding ecosystem and generate strategies tailored to our client's vision. Do you want to know if Equity Crowdfunding is good for you?